Skip to main content

-

Home

-

Letters

-

Scribal

- nar.01971

Ebenezer Rockwood Hoar to George S. Boutwell, 10 July 1869

Image 1

Image 2

Image 3

Image 4

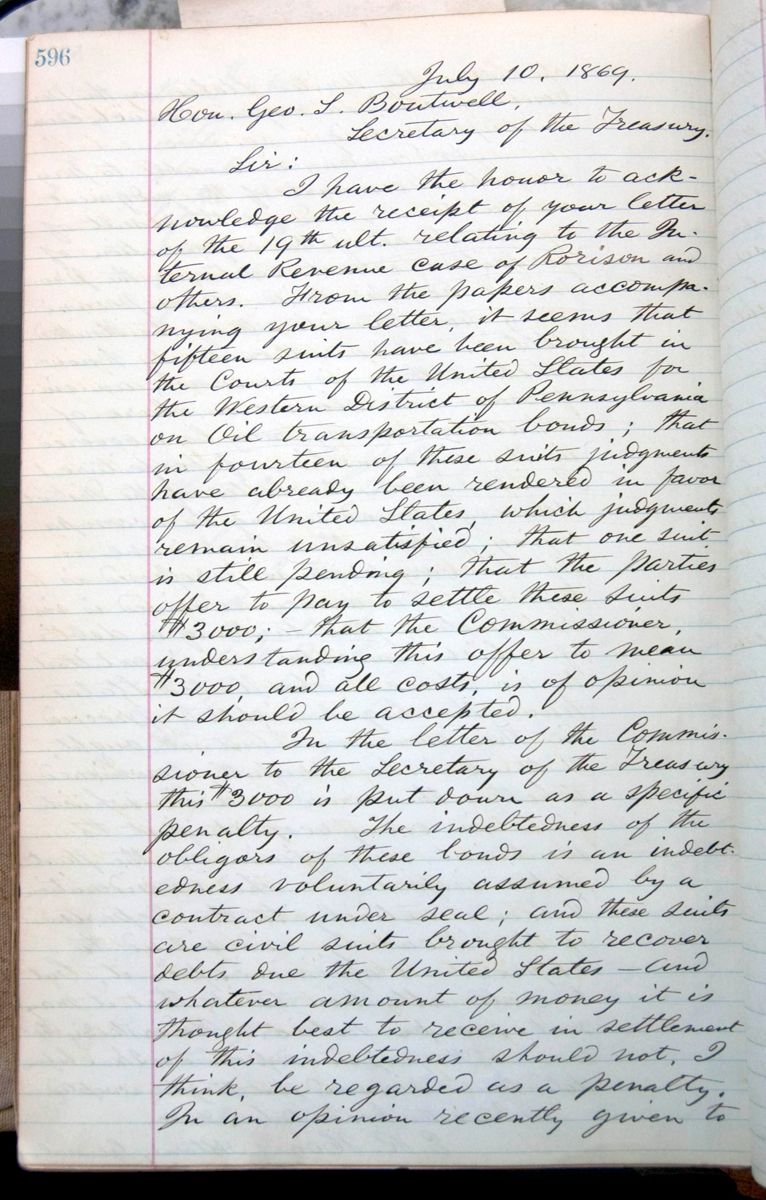

July 10, 1869.

Hon. Geo. S. Boutwell,

Secretary of the Treasury.

Sir:

I have the honor to acknowledge the receipt of your letter of the 19th ult. relating to the Internal Revenue case of Rorison and others. From the papers accompanying your letter, it seems that fifteen suits have been brought in the Courts of the United States for the Western District of Pennsylvania on Oil transportation bonds; that in fourteen of these suits judgments have already been rendered in favor of the United States, which judgments remain unsatisfied; that one suit is still pending; that the parties offer to pay to settle these suits $3000;—that the Commissioner, understanding this offer to mean $3000, and all costs, is of opinion it should be accepted.

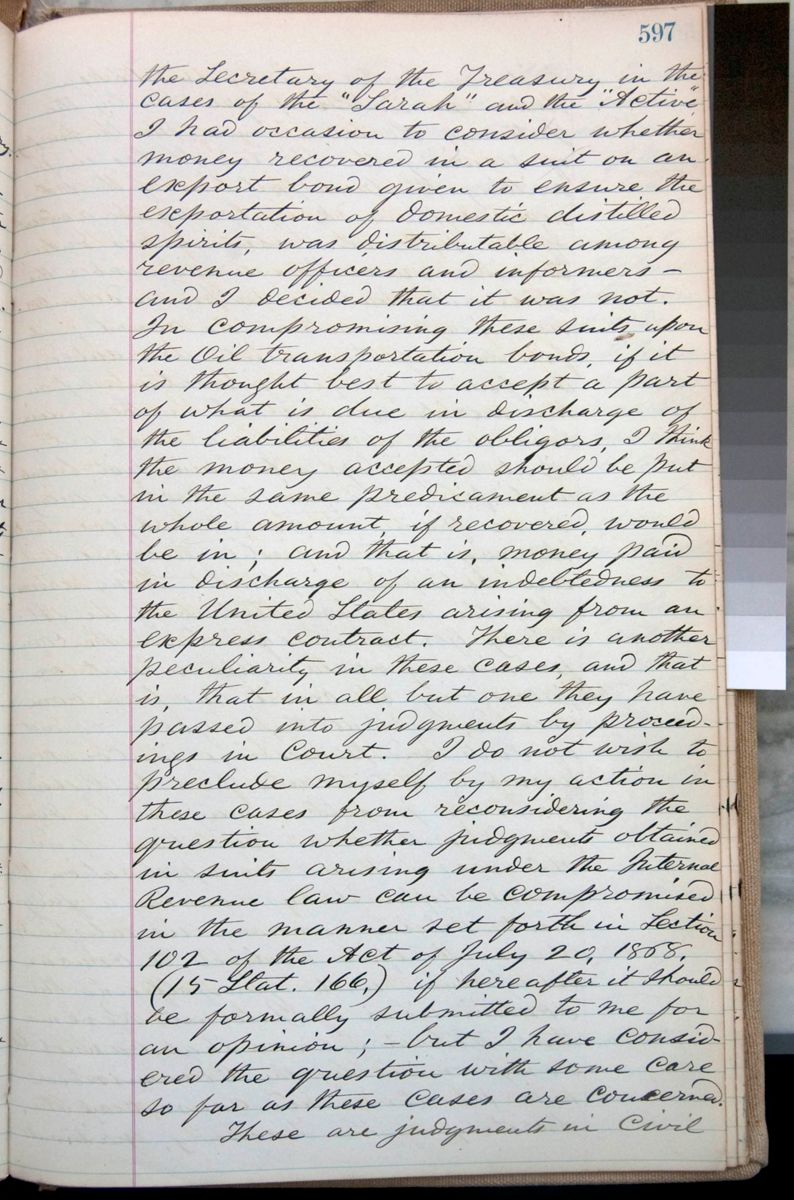

In the letter of the Commissioner to the Secretary of the Treasury this $3000 is put down as a specific penalty. The indebtedness of the obligors of these bonds is an indebtedness voluntarily assumed by a contract under seal; and these suits are civil suits brought to recover debts due the United States—and whatever amount of money it is thought best to receive in settlement of this indebtedness should not, I think, be regarded as a penalty. In an opinion recently given to

the Secretary of the Treasury in the cases of the "Sarah" and the "Active," I had occasion to consider whether money recovered in a suit on an export bond given to ensure the exportation of domestic distilled spirits, was distributable among revenue officers and informers—and I decided that it was not. In compromising these suits upon the Oil transportation bonds, if it is thought best to accept a part of what is due in discharge of the liabilities of the obligors, I think the money accepted should be put in the same predicament as the whole amount, if recovered, would be in; and that is, money paid in discharge of an indebtedness to the United States arising from an express contract. There is another peculiarity in these cases, and that is, that in all but one they have passed into judgments by proceedings in court. I do not wish to preclude myself by my action in these cases from reconsidering the question whether judgments obtained in suits arising under the Internal Revenue law can be compromised in the manner set forth in Section 102 of the Act of July 20, 1868, (15 Stat, 166,) if hereafter it should be formally submitted to me for an opinion;—but I have considered the question with some care so far as these cases are concerned.

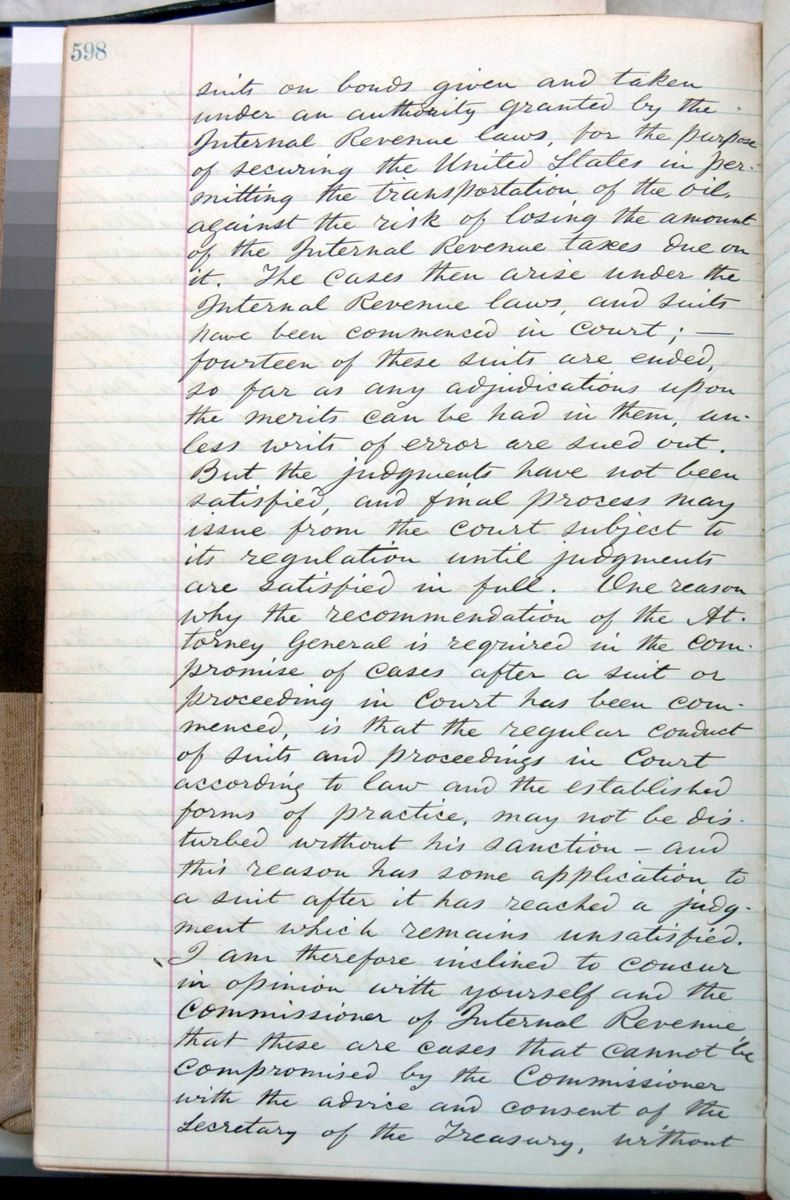

These are judgments in Civil

suits on bonds given and taken under an authority granted by the Internal Revenue laws, for the purpose of securing the United States in permitting the transportation of the oil, against the risk of losing the amount of the Internal Revenue taxes due on it. The cases then arise under the Internal Revenue laws, and suits have been commenced in court;—fourteen of these suits are ended, so far as any adjudications upon the merits can be had in them, unless writs of error are sued out. But the judgments have not been satisfied, and final process may issue from the court subject to its regulation until judgments are satisfied in full. One reason why the recommendation of the Attorney General is required in the compromise of cases after a suit or proceeding in Court has been commenced, is that the regular conduct of suits and proceedings in Court according to law and the established forms of practice, may not be disturbed without his sanction—and this reason has some application to a suit after it has reached a judgment which remains unsatisfied. I am therefore inclined to concur in opinion with yourself and the Commissioner of Internal Revenue, that these are cases that cannot be compromised by the Commissioner with the advice and consent of the Secretary of the Treasury, without

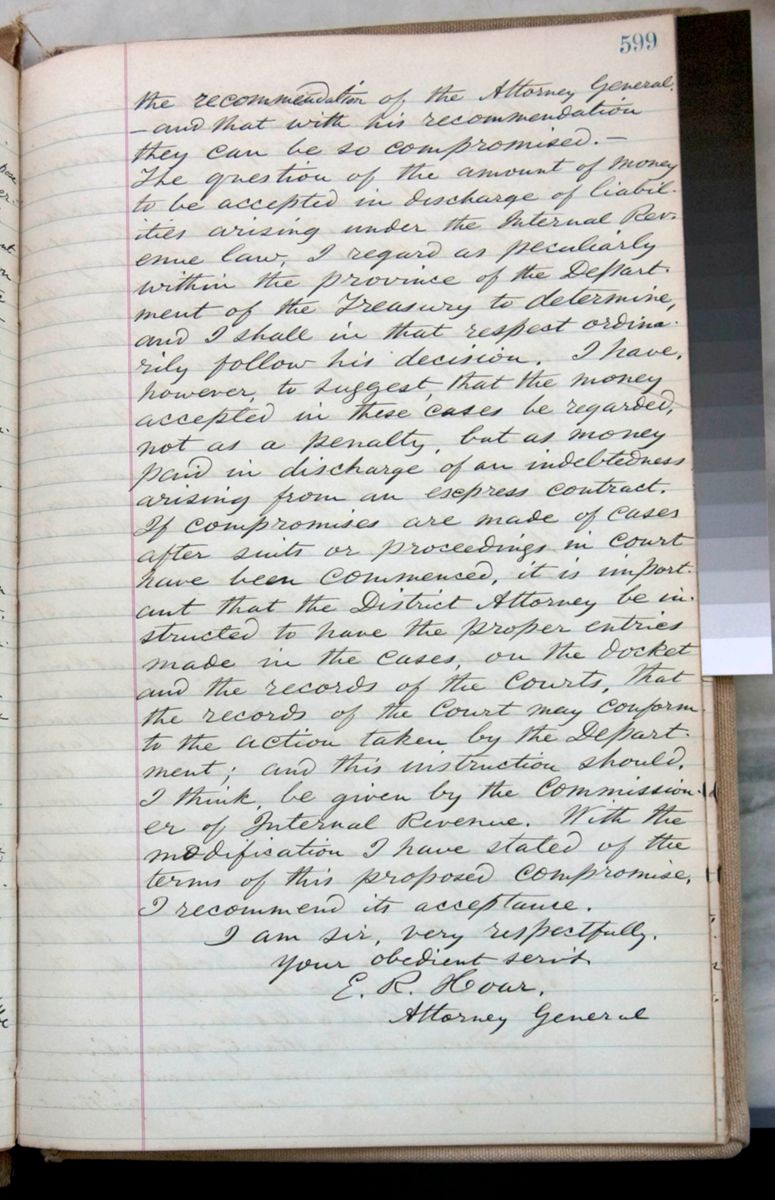

the recommendation of the Attorney General,—and that with his recommendation they can be so compromised.—The question of the amount of money to be accepted in discharge of liabilities arising under the Internal Revenue law, I regard as peculiarly within the province of the Department of the Treasury to determine, and I shall in that respect ordinarily follow his decision. I have, however, to suggest that the money accepted in these cases be regarded, not as a penalty, but as money paid in discharge of an indebtedness arising from an express contract. If compromises are made of cases after suits or proceedings in court have been commenced, it is important that the District Attorney be instructed to have the proper entries made in the cases, on the docket and the records of the Courts, that the records of the Court may conform to the action taken by the Department; and this instruction should, I think, be given by the Commissioner of Internal Revenue. With the modification I have stated of the terms of this proposed compromise, I recommend its acceptance.

I am sir, very respectfully,

your obedient serv't,

E. R. Hoar,

Attorney General